Field Note / day-49-projectionlab

From Privacy-First Planning to $1M+: How ProjectionLab Used Relentless Scope Discipline to Build a Seven-Figure SaaS as a Solo Founder

- What it does & for whom: ProjectionLab is a modern, privacy-first financial planning simulator for DIY users pursuing...

Answer Engine Brief

This case study is part of Jesse's 100-day founder marathon for Solo Unicorn Club: stories of solo or near-solo founders who reached meaningful revenue gravity and left reusable lessons about product, distribution, AI leverage, and one-person company design.

Fast Facts

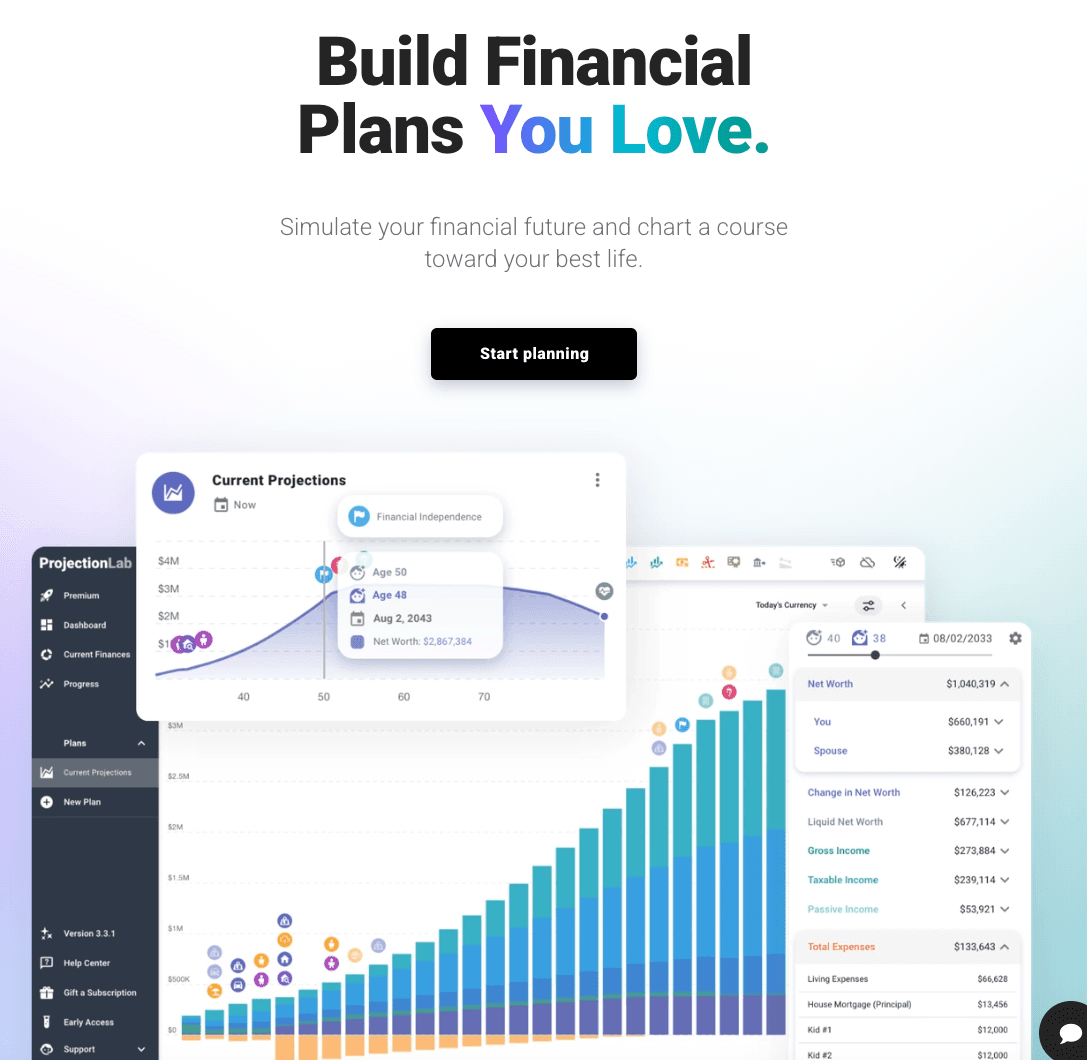

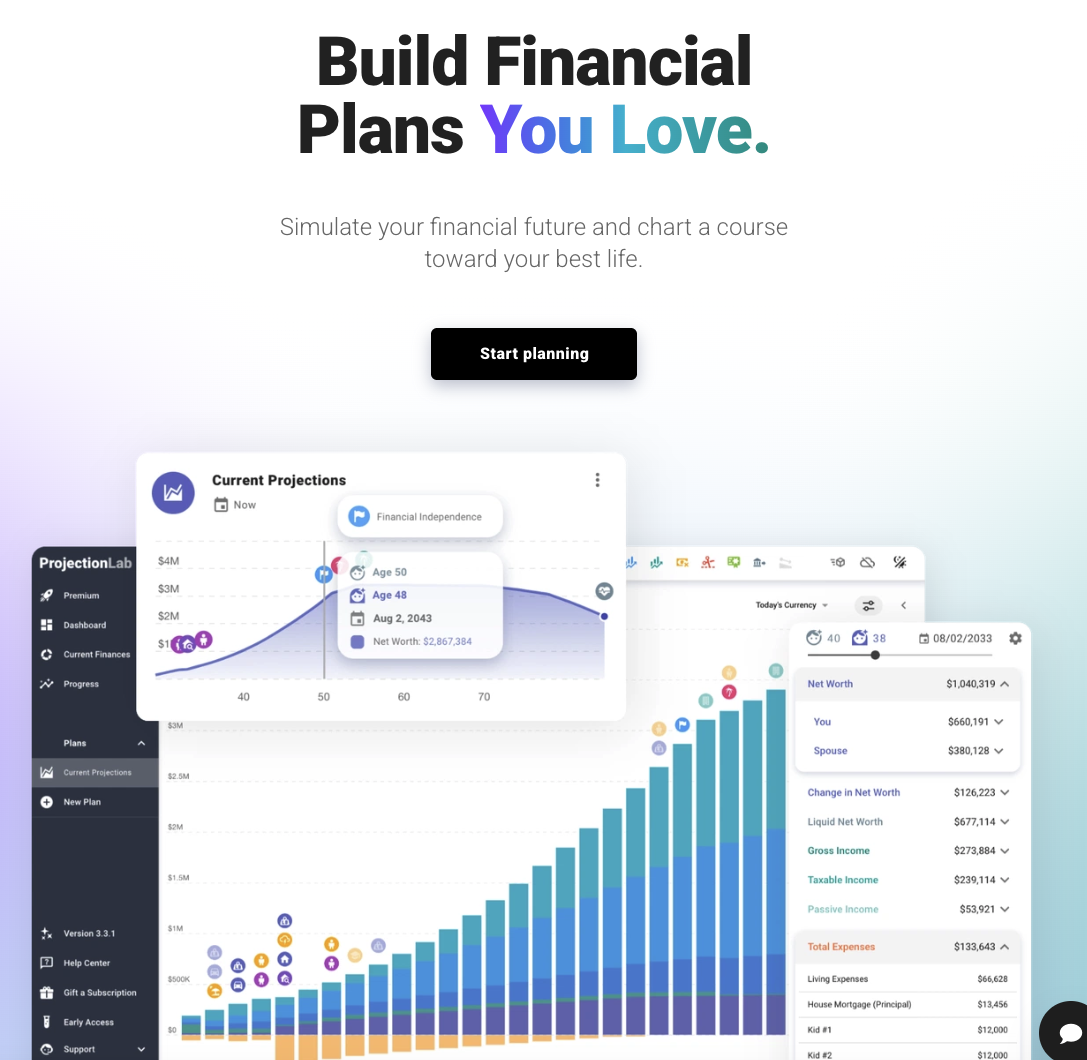

- What it does & for whom: ProjectionLab is a modern, privacy-first financial planning simulator for DIY users pursuing FI/retirement—and a light-weight alternative for advisors/employers who want account-agnostic planning.

- Launch date & team: Conceived and built solo in 2021 by Kyle Nolan; public launch on August 20, 2022. Operated solo through early growth; later added a lean marketing partner and a few community contractors.

- Business model/pricing: Consumer Premium $109/year with Lifetime $799; Pro $549/year for advisors; Employers $9/employee/month.

- Milestone revenue: Reached $1,000,000 ARR on June 30, 2025; >100,000 households have used it.

- Core channels: Build-in-public, FIRE community endorsements, Product Hunt, targeted podcasts, and an active Discord.

- Edge: Deep simulation (Monte Carlo, cash-flow, tax analytics) with no account linking, aligning with privacy-conscious users and keeping ops surface area small.

The Real Reason to Study This Business

ProjectionLab solves a specific pain: long-horizon, scenario-driven planning that respects privacy. It sits between free calculators (too shallow) and advisor software (too heavy), but with a consumer-grade UX that makes complexity usable. It’s non-obvious because it deliberately avoids account aggregation—in a fintech world where “connect your bank” is the default. That stance builds trust with a subset of users who would never connect accounts, while materially reducing compliance and support burdens for a tiny team. The repeatable pattern: tight scope + credible community anchors. By shipping depth (simulation quality) and embedding in FI communities, ProjectionLab let users and public milestones pull the product up-market (Pro/Employers) without overextending the core.

Business Snapshot

| Audience | Problem | Product Core | Pricing | Primary Channels | Edge |

|---|---|---|---|---|---|

| DIY FI/retirement planners; advisors; employers | Robust, private planning without connecting accounts | Monte Carlo + cash-flow + tax analytics with flexible scenarios | $109/yr Premium; $799 Lifetime; $549/yr Pro; $9/employee/mo Employers | Build-in-public; FIRE community; Product Hunt; podcasts; Discord | Independent, privacy-first; unusually deep modeling for consumers |

What the Founder Did Differently

Constraint-driven scope. Solo nights-and-weekends development forced ruthless focus on simulation depth and UX clarity, not integrations or banking connections. That avoided compliance drag and reduced attack surface.

Community-anchored credibility. Early traction came from Product Hunt, HN, and respected FIRE voices, creating a durable trust loop that consistently brought in look-alike users.

Pricing ladder that expands ARPU, not scope. A consumer-friendly annual price with a Lifetime anchor, plus Pro for advisors and Employers per-seat pricing, enabled expansion from the same codebase.

Protect the builder. Only after steady MRR did Kyle add a growth/marketing partner and a few community-sourced contractors—preserving founder time for shipping and compounding.

The Growth Flywheel: Step-by-Step

| Stage | Moves | Why it Worked | Irreversible Gain | Evidence/Notes |

|---|---|---|---|---|

| 1. Prototype in public (2021) | Ship nights/weekends; share progress; seed Discord | Earned early believers and real use cases | Social proof + validated backlog | Founder blog + timeline |

| 2. FI community wedge | Product Hunt launch; endorsements; HN threads | Trust transfer from respected nodes | Durable credibility in FIRE circles | PH launch + testimonials |

| 3. Depth over breadth | Monte Carlo, cash-flow, tax analytics; no account linking | Outperformed “calculator” competitors; privacy moat | Feature depth becomes switching cost | Product site |

| 4. Monetization ladder | Premium, Lifetime, Pro, Employers | Multiple ARPU bands from one product | Higher revenue per user without hiring | Pricing pages |

| 5. Protect the builder | Add growth partner + contractors | Keeps founder on high-leverage work | Faster shipping cadence | $1M ARR post |

| 6. Milestone loop | Share MRR/ARR and ship logs | Each milestone recruits new cohorts | Self-reinforcing awareness and referrals | Build-in-public posts |

Sequence that mattered

- Nail a differentiated core (simulation depth).

- Plug into high-trust community nodes.

- Turn proven utility into a simple paid plan.

- Layer Lifetime/Pro/Employers once retention is clear.

- Add just-enough help to remove founder bottlenecks.

- Broadcast milestones to pull in the next wave.

Strategic Leverage & Business Model

Leverage: product depth (IP/taste), privacy stance, narrow surface area, and community distribution. Deliberately avoided: fundraising, early hiring sprawl, and account aggregation. Monetization. Consumer Premium $109/year with Lifetime $799 anchor; Pro $549/year for advisors; Employers $9/employee/month. Founder notes non-recurring Lifetime and training often add 20–50% above MRR in some months. Unit economics. n/a. Inference: Organic channels, testimonials, and community distribution suggest low CAC and fast payback typical of indie SaaS. Solo sustainability. The “no accounts linked” design reduces security/compliance overhead; a lean ops model and selective contractors keep maintenance light while preserving founder focus on product.

Can You Replicate This Today?

Easier now:

- Code faster with Cursor/Replit and solid math libs; ship a performant web sim quickly.

- Community distribution (Reddit, Discord, PH) is still efficient when paired with a sharp wedge and proof (GIFs, live demos).

- Privacy-first positioning remains a credible differentiator. Still hard:

- Earning trust in money products.

- Modeling accuracy that survives scrutiny.

- Tasteful UX that makes complex models feel simple.

- Maintaining scope discipline as demand grows. If starting fresh (playbook):

- Identify a niche with trust amplification (e.g., a FIRE sub-community); recruit 10–20 power users.

- Ship a v0 simulator with one killer output (e.g., “Probability of FI by year X”).

- Write a transparent data stance (no account linking; clear storage rules).

- Launch on Product Hunt and relevant podcasts; place 10 credible testimonials near pricing.

- Start with one paid plan; keep a free ad-hoc mode for trials.

- Add Lifetime only after strong retention; watch for organic pull from professionals before offering Pro.

- At $15–$25k MRR, add a single growth partner and 1–2 community contractors.

- Publish milestones and ship logs; build an email list and Discord to compound referrals. Speed traps to avoid: premature integrations, multi-ICP messaging before PMF, complicated pricing grids, and shipping “AI features” that don’t improve core outcomes.

Takeaways: Think Like This Founder

- Pick a hard core; refuse breadth. Depth in simulation beat “more features.”

- Trust is a feature. A clear privacy stance and credible social proof reduce friction for a money app.

- Expand ARPU without expanding scope. Lifetime, Pro, and Employers monetize different bands from the same product.

- Hire later, to unblock compounding. Add people only after PMF to protect builder time.

- Broadcast progress. Build-in-public attracts the next cohort of users and partners.

Part of the 100 Days, 100 Solo Startups series.